Old Before Rich

China is getting old before it gets rich. The danger to Australia gets bigger before it gets smaller.

By James Kell

Beijing announced a 3,600-yuan-per-child subsidy in 2025, payable for the first three years of a child's life. That is about $750 Australian a year. It is the price the Chinese state has put on a child it would prefer be born. Singapore has tried larger subsidies for twenty years, and its fertility rate is 0.87. South Korea has tried larger subsidies for thirty, and its fertility rate is below 0.7. The lesson Asia has already taught – that ultra-low fertility, once embedded, is not policy-responsive – is the lesson Beijing is now beginning to learn at scale.

Numbers like 0.87 and 0.7 do not sound dramatic. They are. To hold a population steady, a country needs about 2.1 children per woman – two to replace the parents, a fraction more to cover children who do not reach adulthood. That figure is the replacement rate. Below it, a population shrinks. Sustained below it, a population trends to zero.

The arithmetic compounds quickly. At a fertility rate of 1.0, each new generation – about thirty years – is roughly half the size of the one before. At 0.7, the rate South Korea now has, each new generation is roughly one-third. Sustain that for four generations – about a hundred and twenty years – and the starting cohort is down to about one-eightieth its original size. The ordinary remedy is mass immigration. China, for political reasons that are unlikely to change, cannot run that remedy at the scale required.

That is the visible part of the story. The numbers behind it are what should change Australian thinking.

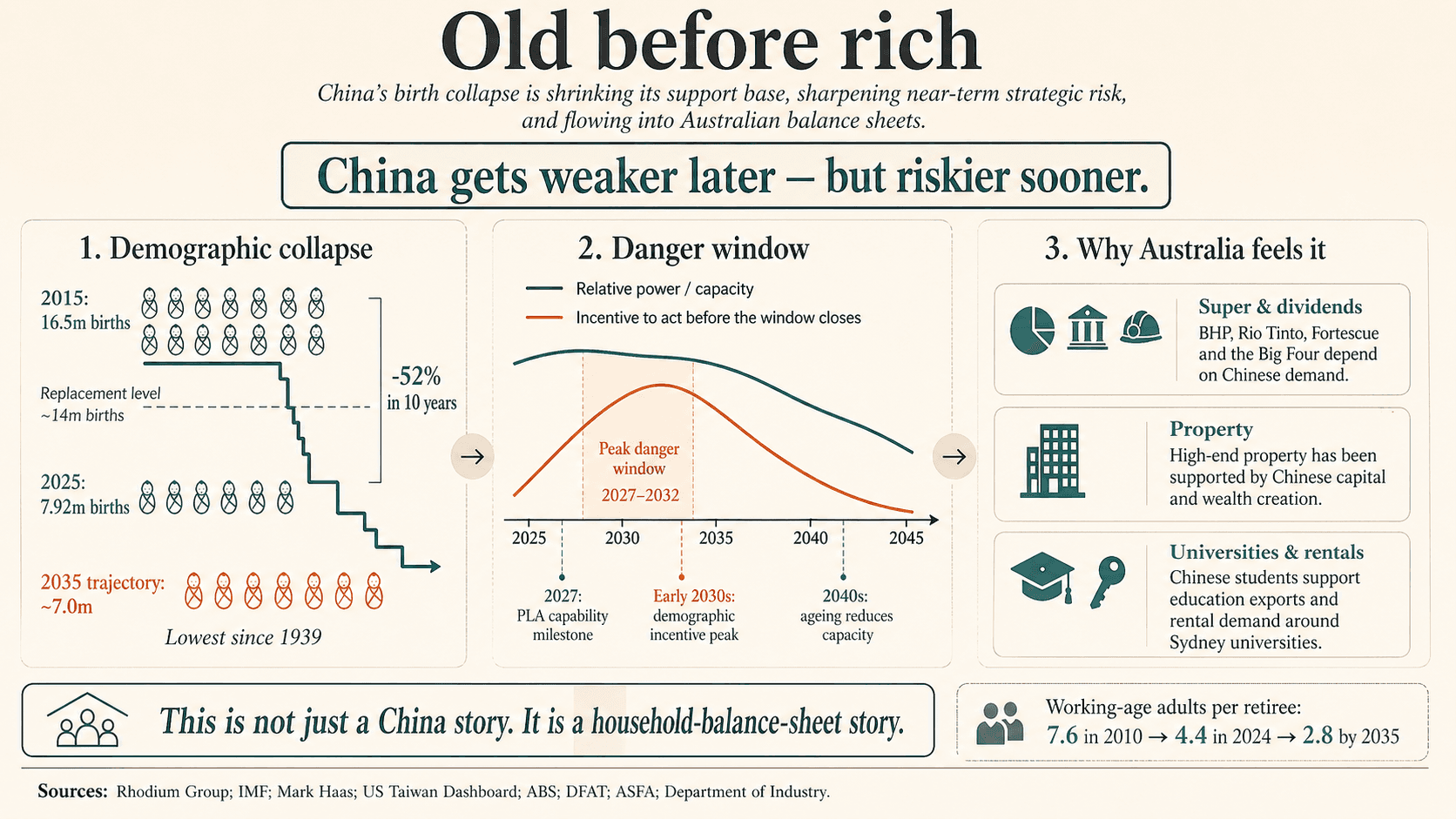

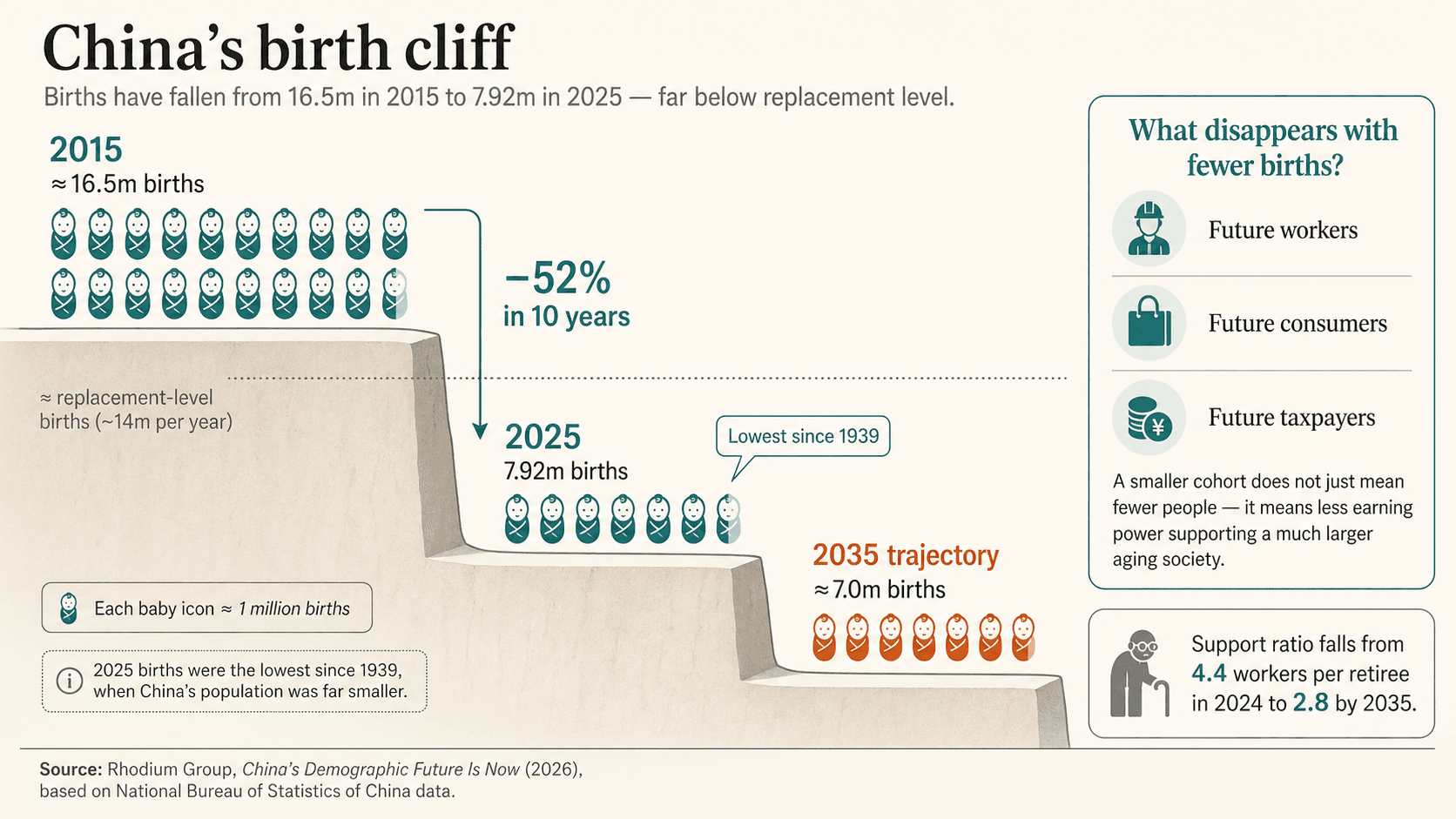

In 2025, China recorded 7.92 million live births – the lowest in any calendar year since 1939. 1939 is not a number chosen for emphasis. It is the calendar year. China's population in 1939 was around 510 million. China's population today is 1.4 billion. The country is now recording fewer births than it did when it was a third its present size. The independent demographer Yi Fuxian, who first proved Beijing was systematically over-counting its population, argues that even the 7.92 million figure is too generous; his correction puts the real number closer to 7.4 million. The point is not which figure is right. The point is that the error bar runs in one direction. Local Chinese officials face career penalties for under-reporting growth and for over-reporting demographic decline. The candid reading of the data is that the central case is bad, the upside scenarios do not exist, and the downside scenarios are worse.

Michele Wucker calls this a grey rhino: the danger that has been visible for years, while everyone agrees not to act on it, until it is charging. The opposite of a black swan. Black swans are by definition unforeseeable. Grey rhinos are the things we could see all along.

For a Wentworth reader who wants the short version: China is shrinking, the shrinking is real, and the shrinking does not make us safer. The same arithmetic that makes China weaker by 2045 also makes it more dangerous between now and the early 2030s. Whether Australia carries insurance against that decade is the choice the next government will make. The rest of this essay is the case for the insurance, and what it should buy.

I. The data, plainly

Australia is at 1.48. Most of Europe sits between 1.3 and 1.6. Japan is at 1.2. South Korea is below 0.7. Singapore is at 0.87. China, on its own official numbers, is around 1.0; Yi Fuxian's correction puts it lower. Every country in that list is, on the arithmetic alone, slowly shrinking. China is the only one in that list that cannot offset the shrinkage with new arrivals.

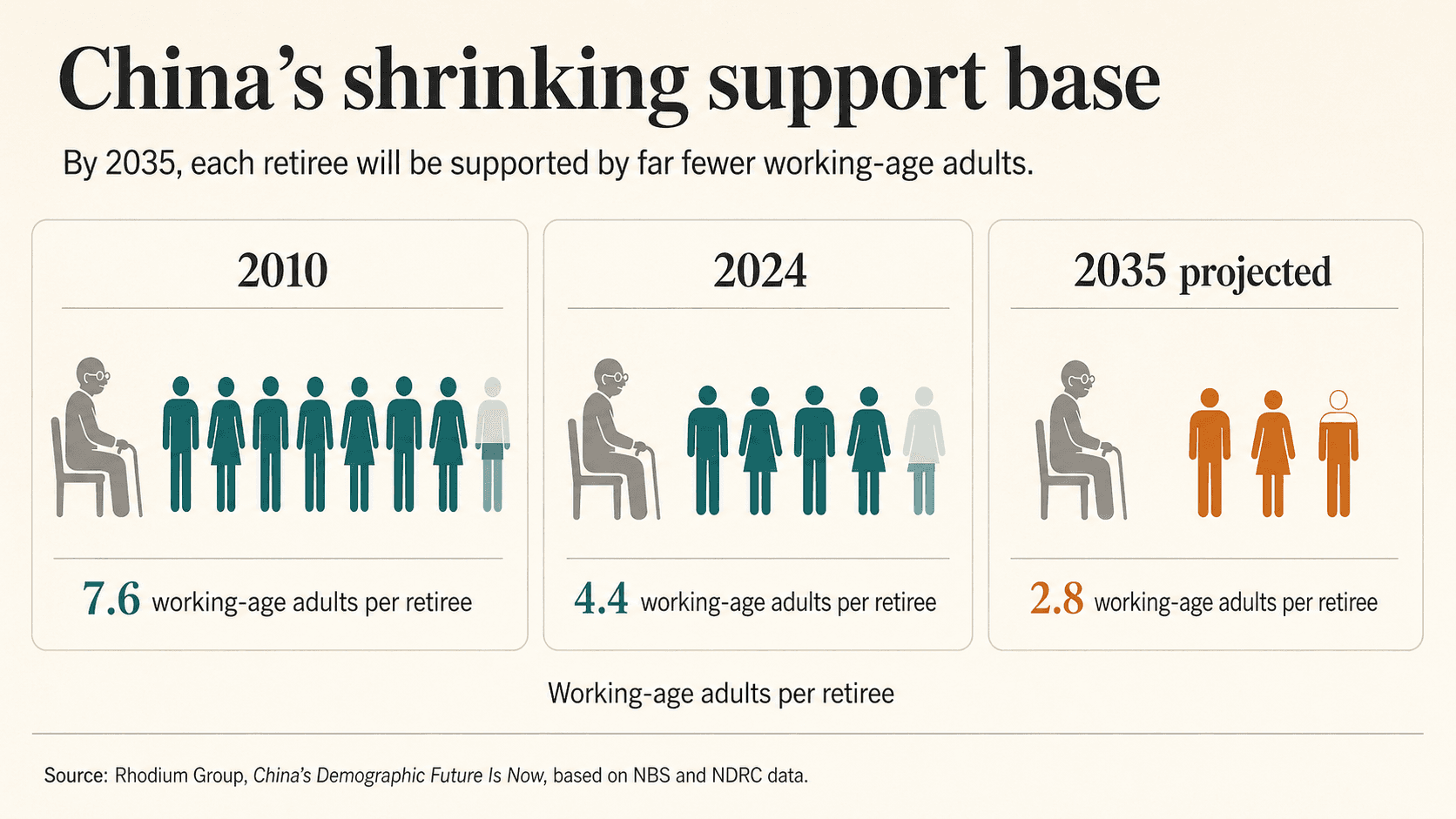

The next number is the dependency ratio – the number of working-age adults supporting each retiree. In 2010 the ratio was 7.6. By 2024 it was 4.4. By 2035 it will be 2.8. In plain language: where almost eight working-age Chinese adults supported each retiree fifteen years ago, by 2035 there will be fewer than three. China is on course to lose, in twenty-five years, two-thirds of the working-age cohort it once had per retiree. China's pension system was not built for that arithmetic.

Set those numbers alongside the headline findings of the Rhodium Group's April 2026 report, China's Demographic Future Is Now:

- Net population decline of 3.4 million in 2025 – more than double 2024's loss; projected to widen to 7.6 million a year by 2035.

- Women of childbearing age have fallen 13 per cent in a decade, to 213.7 million.

- Marriages are down 40 per cent since 2018, to 6.1 million a year.

- The fiscal subsidy to China's social-security funds in 2025 was 2.9 trillion yuan, or 10.1 per cent of the entire general budget. Without it, the system runs a 1.4 trillion yuan deficit.

Read those four lines together. China is losing population faster every year. The women who would have had the next generation are already gone. The young are not marrying. And the social-security books are kept solvent only by a fiscal subsidy worth a tenth of the entire central budget. None of these lines is bending in a direction that helps.

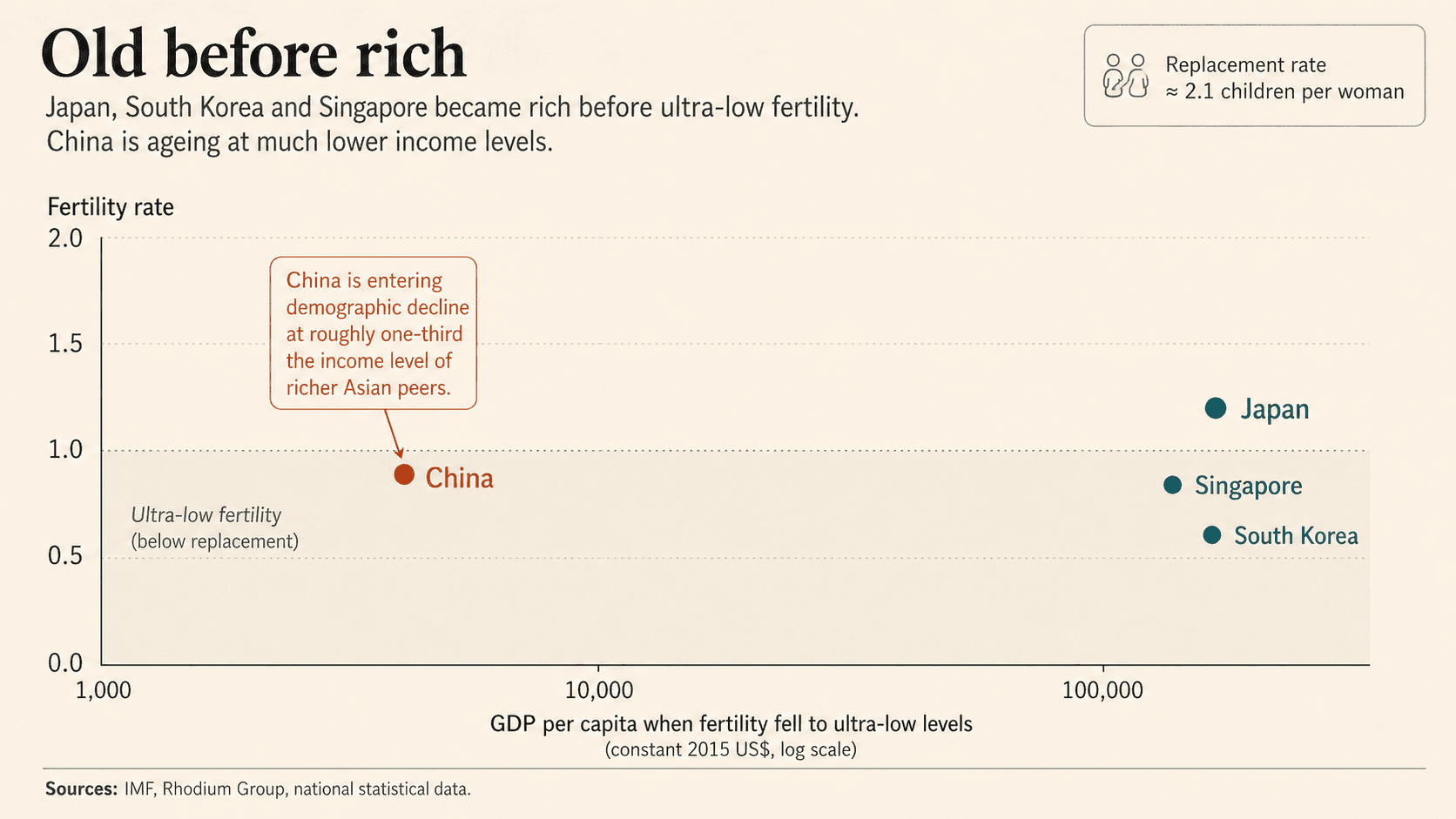

The IMF's framing of all this, from its 2017 Asia Regional Economic Outlook, was a question in a title: was the continent at risk of "growing old before becoming rich"? Japan and South Korea hit ultra-low fertility at GDP per capita above $40,000. China is hitting it at roughly $13,000. The IMF estimates ageing alone will subtract between half and three-quarters of a percentage point from China's annual GDP growth for the next thirty years. China is the first great power in modern history attempting national rejuvenation while becoming an old country before it becomes a rich one.

The plain version: Japan, South Korea, and Singapore got rich first, then aged. China is ageing on the way up. That is what old before rich means. No country of China's size has ever been in this position before.

This trajectory is not opinion. It is the demographic equivalent of an iron law: once the cohort of women aged 22 to 34 has shrunk, no policy reverses the cohort. The babies who would have been born in 2040 are decided in 2026. And the dividend cheques on which Wentworth's retirees expect to draw in 2040 are priced off the same decision.

II. The paradox Australian policy refuses to face

The conventional reading of these numbers is comforting and wrong. China is shrinking, runs the argument, therefore China cannot project power, therefore Australia can relax. That reading has the right destination – China is, on the long horizon, becoming materially weaker – and the wrong route to it.

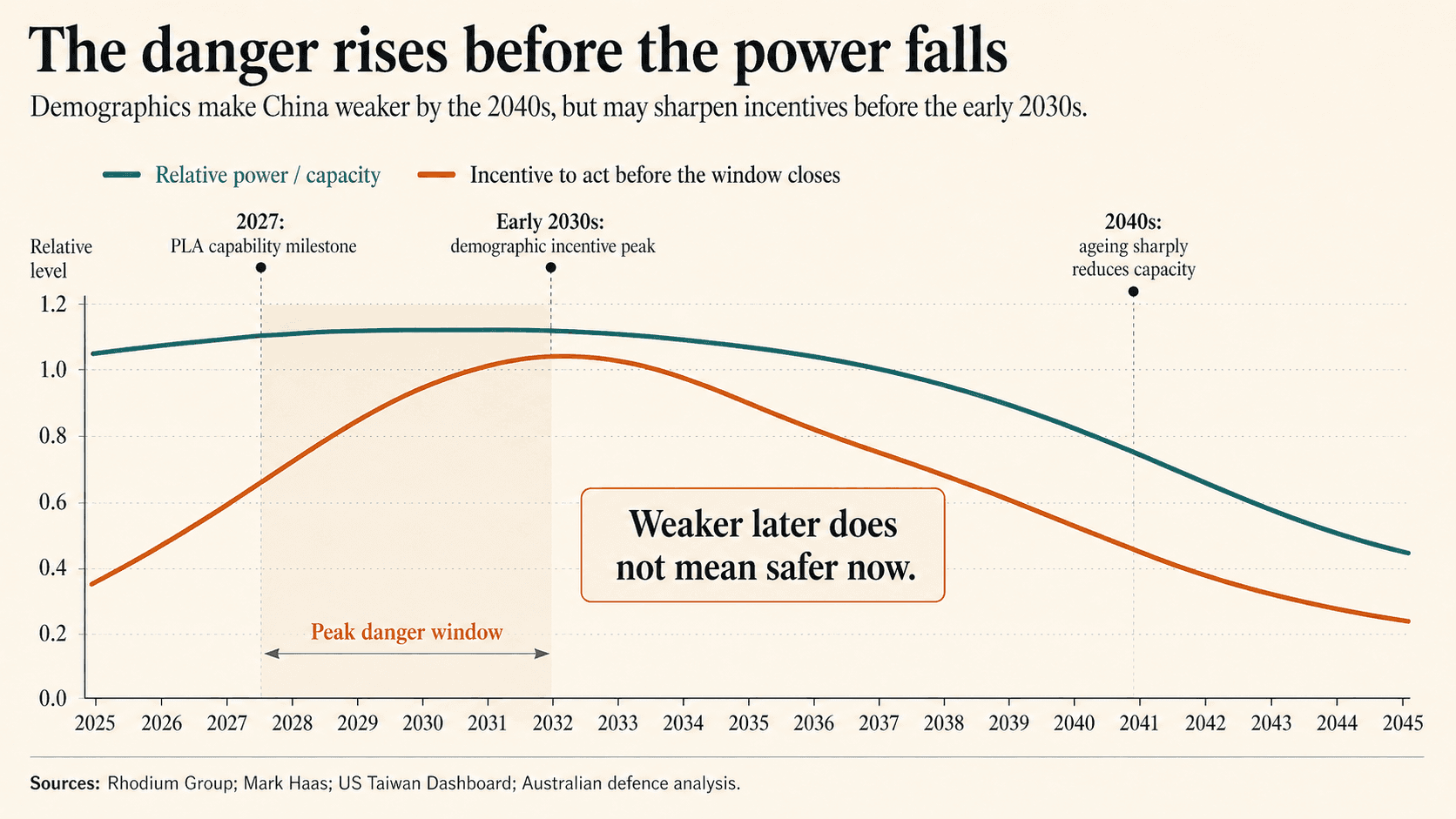

The political scientist Mark Haas, whose work on age and great-power conflict is cited in the United States Department of War's Xi Jinping's Taiwan Dashboard (April 2025), puts the long-run case plainly: "Because of high life expectancies and extraordinarily low fertility levels, China is aging faster and to a deeper extent than any other great power, and possibly any country, in history. Aging significantly reduces states' capacity to aggress." Haas is right about the destination. By 2045, China will not be capable of the foreign policy it can run today.

The same paper notes that of thirteen indicators driving Beijing's calculus on Taiwan, eleven point toward earlier action. Xi Jinping reads the same data Rhodium publishes. He understands that his window of relative power closes in the early 2030s. The serious literature on Beijing's strategic horizon has been clear for some time on what this implies. Demographics make China weaker by 2040. Demographics make China more dangerous between 2027 and 2032. Both can be true. Both are.

That is the paradox at the centre of this question, and Australian policy has not faced it. The Albanese government's 2026 National Defence Strategy, released on 16 April 2026, does some of the work. It accepts the older, harder language of balance of power – the idea that peace is held by countries balancing each other's strength – rather than the friendlier "rules-based order" formulation of 2024. It commits to defence funding rising to 3 per cent of GDP by 2033. It is the most strategically literate document the Commonwealth has published in two decades. It is also too slow, by a margin set in Beijing.

The implication is not that Australia should adopt a war footing. It is that we should stop running policy as if we had all the time in the world. Stabilisation is a tempo choice, not a strategy. The tempo is being set in Beijing, and Beijing is now operating against a clock its leadership cannot stop.

III. The voices selling the comfortable story

Search any Australian newspaper this month for the phrase "China's demographic challenges are overstated". You will find a small cluster of names. Geoff Raby, the former Australian ambassador to Beijing, appears on the ABC and in the Australian Financial Review arguing for warmer relations with China. James Laurenceson, director of the Australia-China Relations Institute at the University of Technology Sydney, is the lead author of the institute's February 2026 paper telling Australians that the iron-ore relationship with China will hold even as Beijing brings on alternative supply from the Simandou deposit in Guinea. The columns this month telling Australian readers that the Chinese economy is more resilient than the headline numbers suggest, that demographic decline will not be as steep as Yi Fuxian forecasts, that Beijing's response will be more sophisticated than the West expects – the same names tend to be on them.

This is not illegal commentary. It is also not neutral commentary. Raby is registered under the Foreign Influence Transparency Scheme, on his own initiative under Australian law, because he sits on the board of Yancoal, an Australian subsidiary of a Chinese state-owned coal company. ACRI was founded in 2014 with a $1.8 million donation from Huang Xiangmo, a Chinese property developer barred from re-entering Australia in 2019 on ASIO advice. Bank of China and China Construction Bank are listed as institute donors. The full audit of ACRI's funding is set out in Australia's China Problem on this site.

The point is not to ban any of this. The framework already exists, was passed by an Australian parliament in 2018, and has been tested and upheld in the courts. It was designed precisely for what is happening now – foreign-influenced commentary, lawfully published, on a question of Australian national interest. What the framework does not yet do is plain-English disclosure on the screen and in the byline. When a man whose own legal obligations require him to register as an agent of foreign influence appears on national television arguing that the Chinese economy is stronger than the data suggests, that disclosure should be on the screen the whole time he is speaking. The viewer has standing to know who is paying for the comfort.

IV. Non-zero, and the case for insurance

Whatever probability a careful analyst assigns to a scenario in which Beijing acts on Australian sovereignty in the next decade – through coercion, dependency capture, information warfare, or some combination of these – is not zero. The Rand Corporation, the United States Studies Centre, ASPI, the Lowy Institute, and the Defence and Foreign Affairs portfolios within Canberra differ from each other by a factor of three or four on the size of the risk. None of them assigns zero.

When probability is non-zero, you buy insurance. This is the most familiar logic in Wentworth. Households here insure their houses against fire, their cars against theft, their bodies against illness, their professions against negligence claims. They do not refuse to think about the chance of fire because thinking might cause one. They put a premium aside, recalculate it annually, and treat the cost as the price of being a serious adult about a low-probability, catastrophic outcome.

National security is the same problem at a different scale. The probability of catastrophic loss is not zero. The premium is the cost of preparation. The argument that talking about it makes it more likely is the argument of someone who has not thought about the mechanism.

Beijing's posture is not set by Australian commentary. The Chinese military's 2027 capability milestone – the year by which the People's Liberation Army is meant to be able to take Taiwan if ordered – was selected in 2017, before any Australian sentence on this topic was published. The Chinese Communist Party's overseas-influence operations in Australia run on a timetable Beijing controls. The probing of Australian critical infrastructure that ASIO Director-General Mike Burgess described to the National Press Club on 11 November 2025 is happening regardless of what is on the front page of the Sydney Morning Herald. Australia is simply not a strong enough variable in Beijing's planning for our domestic conversation to move it.

Engagement-era silence has been tested for twenty years. It was a mirror, not a sedative. The thing it was supposed to do – soften Beijing's behaviour, restrain its territorial ambition, embed it in liberal norms – did not happen. In every direction the trajectory was the same. South China Sea: more islands, more militarisation. Hong Kong: National Security Law, 2020. Xinjiang: surveillance state. Taiwan: more aircraft, more incursions, more ships. Australia: economic coercion in 2020, infrastructure probing now. The dragon was already awake. Our silence did not put it to sleep.

The premium on insurance looks expensive in good weather. It looks cheap after the storm.

V. Why this hits Wentworth, specifically

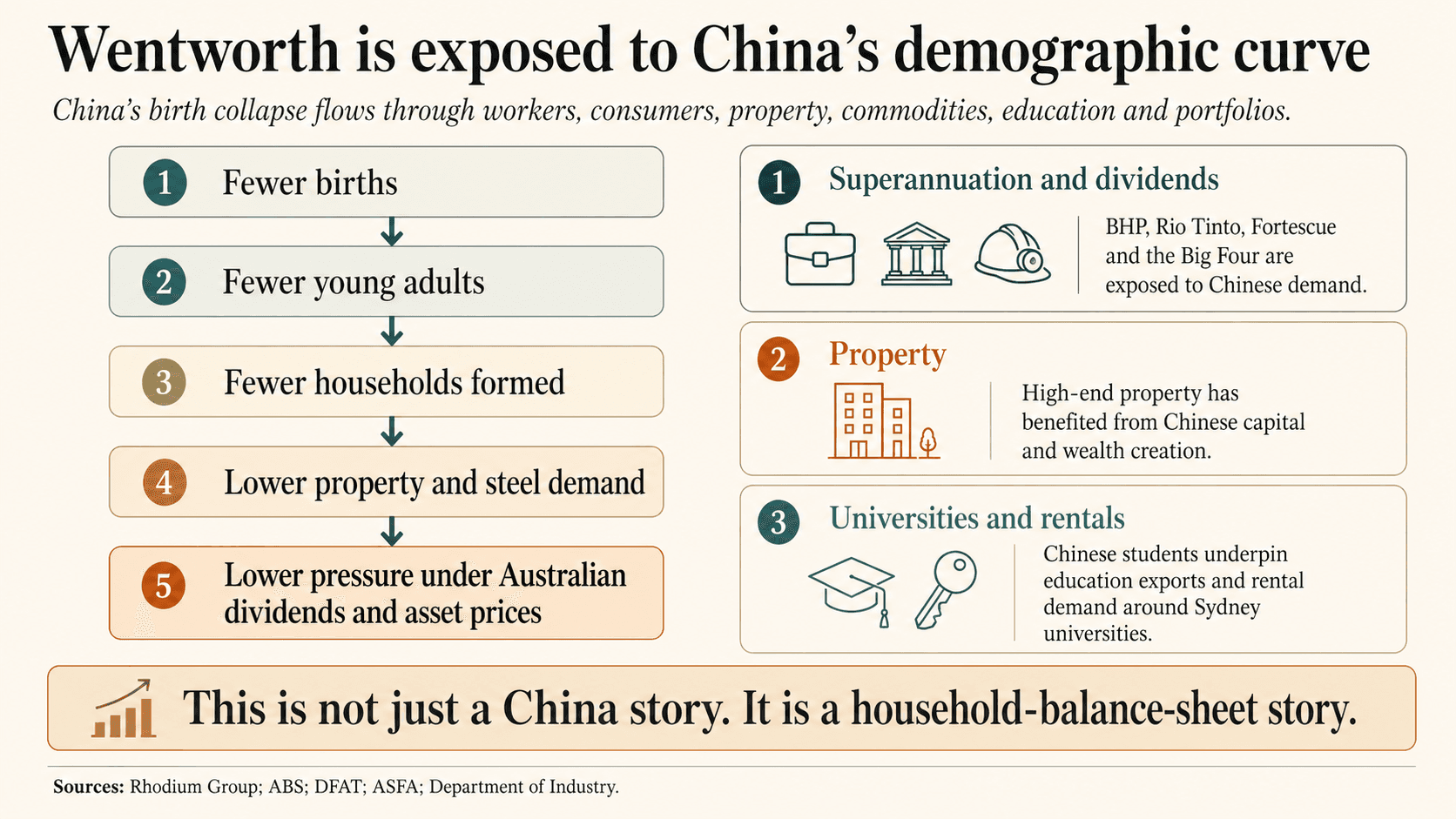

There is no electorate in the country more financially exposed to the curves in those charts than this one.

The average superannuation balance in Wentworth is around $368,000, the highest in Australia. Those balances sit on top of BHP, Rio Tinto, Fortescue, and the Big Four banks. The long-run dividend assumptions priced into those holdings are downstream of Chinese steel demand. Steel demand is downstream of property starts. Property starts are downstream of household formation. Household formation is downstream of women aged 22 to 34. That number is already down 13 per cent. A Bellevue Hill retiree drawing on a balanced fund holds, whether they realise it or not, a concentrated bet on the cohort of Chinese women who decided not to have a second child between 2018 and 2025.

Sixty-nine per cent of dwellings in this electorate are units. Two decades of Chinese capital have priced the high end of the market – the trophy harbour-side apartment, the Vaucluse renovation, the Double Bay penthouse. The buyer base is now ageing in lockstep with the cohort that built that wealth. The pipeline narrows from here.

Some 24.7 per cent of Australia's education exports come from Chinese students, funnelled overwhelmingly through the University of New South Wales and the University of Sydney. Both universities anchor this electorate's catchment for staff, alumni, and rental demand. The cohort of Chinese eighteen-year-olds will start contracting sharply in the late 2030s. The dependency is on a curve that does not bend.

Wentworth is also one of the most foreign-policy-attentive electorates in the country. The first organisation listed under the Foreign Influence Transparency Scheme, in 2023, was a Chinese Communist Party United Front body. The first criminal conviction under the 2018 foreign-interference laws – of Di Sanh Duong, sentenced to two years and nine months – involved an attempt to influence a federal minister in favour of CCP positions. The voters in this seat did not need either case explained to them when it landed. They will not need this one explained either.

The Wentworth voter is not a passive observer of the Australia-China relationship. They are paying for it through their portfolio, their property, and their schools. They have, more than most Australians, the right to demand a government that carries insurance.

VI. What insurance buys

Three things, in plain English. None of them prejudges the answer to the strategic question. All of them are premiums.

One. A whole-of-system scenario register, tabled annually.

Not the Taiwan-cost number alone (that ask sits in Australia's China Problem). The bigger discipline. An annual document, tabled by the Treasurer, signed off by Treasury, the Reserve Bank, Defence, Home Affairs, and the Office of National Intelligence, modelling what an old-but-dangerous-decade costs Australia across every portfolio. Trade. Energy. Education. Migration. Insurance. Health. Defence. Cyber. Critical infrastructure. The Australian public is entitled to a document that reads as if its writers had thought, together, about what 2027 to 2035 might require. No serious country runs blind on its largest strategic risk, and no serious electorate should accept a government that does.

Two. Critical-minerals processing capacity onshore or with allies, to a hard date.

Not a target. A date. The Critical Minerals Production Tax Incentive was legislated in 2025. The Critical Minerals Strategic Reserve becomes operational in late 2026. Iluka's Eneabba refinery is due to deliver separated rare earths from 2026. These are directional. They are not yet a date by which a stated share of Australia's lithium, rare-earth, gallium, and graphite throughput will be processed outside Chinese control. A date is the difference between a strategy and a wish. Pick one. Publish it. Stand on it.

Three. Plain-English foreign-influence disclosure, every time.

One line, on the cover of every paper, in the chyron of every television appearance, in the byline of every op-ed by anyone publishing on Australian China policy: "This author is registered under the Foreign Influence Transparency Scheme", or "This institution receives funding from [list]". The framework already exists. It is currently enforced in the breach. Make it enforced in the use. The viewer, the reader, the student, and the policy-maker is entitled to that information at the point of contact, not retrospectively in a footnote on page nine.

These are insurance premiums. They cost relatively little to put in place. They produce outsized protection if the worst version of the next decade arrives. They produce useful discipline even if it does not.

VII. The window

Robert Menzies, in The Forgotten People in 1942, wrote that the foundation of national strength was the citizen who had thought, calmly, about what their country was holding and what it might cost to defend. Menzies was speaking in a year in which the answer to that question was already being paid in lives.

The country that knows what it is holding pays the premium calmly. The country that does not, pays the full claim later.

Discussion does not wake the dragon. The dragon was already awake. What our discussion can do is decide whether we meet it prepared, or whether we meet it the way the country in 1939 met the consequences of a decade of pretending things were going to be fine.

It is 2026. 2027 is the capability date. The early 2030s is the demographic incentive peak. The window between today and that peak is six years – fewer than the time it takes to build a frigate, to train a generation of Mandarin-capable analysts, or to stand up a critical-minerals refinery. The premium has to start being paid now.

Sources

- Rhodium Group, China's Demographic Future Is Now, April 2026.

- Yi Fuxian, public corrections to Chinese fertility and birth data, 2024–2026; Newsweek, "How China's Birth Rate Compares With the World", January 2026.

- International Monetary Fund, Regional Economic Outlook: Asia and Pacific – Asia: At Risk of Growing Old before Becoming Rich?, October 2017.

- Mark L. Haas, "A Geriatric Peace? The Future of U.S. Power in a World of Aging Populations", International Security, Vol. 32, No. 1, Summer 2007.

- United States Department of War, Xi Jinping's Taiwan Dashboard, April 2025.

- Lowy Institute, China, Taiwan, and the PLA's 2027 milestones, February 2025.

- Australian Government, Department of Defence, 2026 National Defence Strategy and Integrated Investment Program, 16 April 2026.

- Australian Strategic Policy Institute, Strategist commentary on NDS 2026, April 2026.

- Bloomberg Economics, "Taiwan Strait Conflict Would Cost Global Economy $10 Trillion", January 2024.

- Australia-China Relations Institute, University of Technology Sydney, Leverage in the Australia-China iron ore trade, February 2026.

- The Conversation, "The Australia-China Relations Institute doesn't belong at UTS", June 2017.

- University of Technology Sydney, ACRI Funding disclosures.

- Commonwealth of Australia, Foreign Influence Transparency Scheme Public Register.

- Commonwealth Director of Public Prosecutions, case report, R v Di Sanh Duong, 2024.

- Australian Security Intelligence Organisation, Director-General's address to the National Press Club, 11 November 2025.

- Australian Bureau of Statistics, International Trade Supplementary Information, Calendar Year 2024.

- Department of Industry, Science and Resources, Resources and Energy Quarterly, December 2024.

- International Energy Agency, Global Critical Minerals Outlook 2024.

- Department of Foreign Affairs and Trade, China Country Brief.

- Association of Superannuation Funds of Australia, Superannuation account balances by region research note.

- Michele Wucker, The Gray Rhino: How to Recognize and Act on the Obvious Dangers We Ignore, St. Martin's Press, 2016.

- R. G. Menzies, The Forgotten People broadcast address, 22 May 1942.